Teens & Money

Helping your teen build a healthy relationship with money is one of the most valuable gifts you can give them. But let’s be honest—teens don’t always see the bigger picture when it comes to finances. That’s where we come in.

Through Financially Empowered for Teens, your teen will learn how to:

Connect their spending habits to their dreams and goals

Understand the value of money through fun, real-life activities

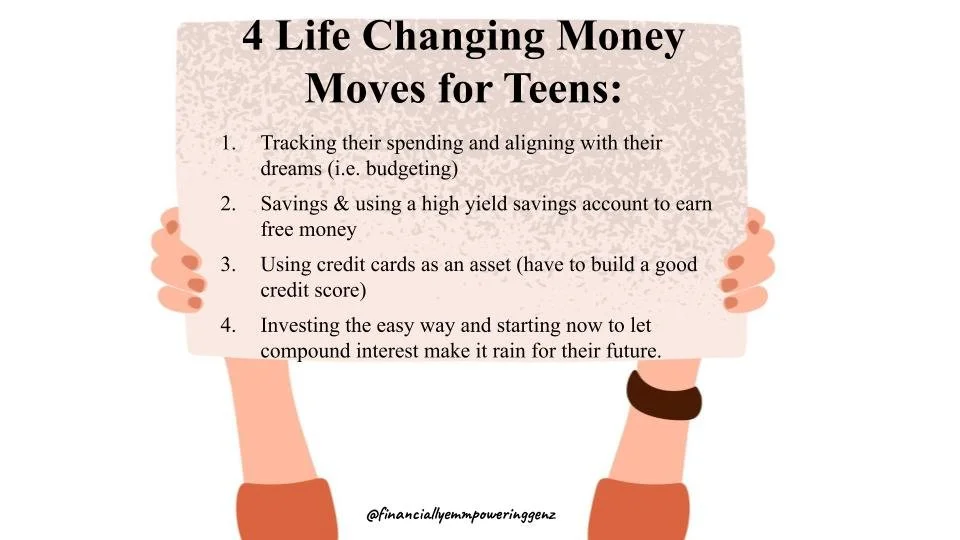

Master 4 life-changing money moves that will ignite their future

2 Ways to Empower Your Teen’s Financial Journey:

#1: Enroll your teen in the class and let them take charge of their own money transformation.

They’ll engage in an independent, interactive program designed to give them the skills and confidence to build a thriving financial future.

#2: Enroll in the Parent’s Class and lead your teen’s financial journey.

This option is designed for parents who want to take a more hands-on role. You’ll learn the tools, strategies, and activities to teach and guide your teen with my support every step of the way.

While option #1 allows your teen to independently own their financial growth, many teens benefit from additional guidance—which is why we’ve created option #2 to empower you as their financial mentor.

Give your teen the tools to dream big, take control of their finances, and create a future they love. Let’s make it happen together!

Full Course Details Here

If you aren’t ready to jump into the full course, you can start with the Value of Money activities (FYI, this is included in the classes above)

Cost: $97

Does your kid or kids struggle to understand the value of money?

I get it.

Navigating your teen's financial education is a wild ride, battling their craving for instant gratification and the peer pressure of consumer culture. Money smarts is a tightrope act that most teens fail to grasp yet is vital for them to thrive in adulthood. Despite your efforts to preach hard work and prudent spending, the struggle to impart the value of money remains a significant challenge.

Here is where I come in. I work with teenagers every day in my Personal Finance class. I developed these 5 activities to start engaging teens with their future and the connection money has to that future. These activities are fun and have immediate buy in for young people because it is a tangible and realistic way to channel their independence and engage with their future.

In these 5 activities, teens are going to build their dream budget. In order to make this happen, they are going to do 3 supporting activities: Housing, Car, Food. Your teen will research housing and learn about take home pay and how much they should be spending on housing. They will research their dream car, mid price car and cheaper option and ultimately discover the monthly payment. For food, teens will put together a meal plan for eating in and buying out. Then they will bring all of this together to calculate how much they would need to make to live their dream life. This is all the fun stuff.

Lastly, teens will complete a starting budget of $55,000 which is usually substantially lower than the number on their dream budget. This brings kids back down to reality as they have to calculate student loan payments, have to save and invest in this budget. Most teens find this activity to be a struggle as they are faced with the harsh reality that $55,000 does not go that far and the many cuts they will have to make to live within this budget. This is when they truly start to grasp the value of money and the role it will play in their life. See below for quotes from my students after doing this bundle of activities.

Each activity comes with video instructions.

Cost: $97

The education system fails to teach the essential money skills to thrive in adulthood. I am a high school personal finance teacher teaching the money moves that empowers young people to ignite their dreams.

Impact on students …

“I was shocked when I realized I was around 3k above the limit. I had to cut a ton of costs to make it to the limit which was tough. I had to get rid of my car and rely on public transportation which is a big loss. This made me realize that it’s harder to live the life I want than I thought. Almost all of my money goes to necessities and hardly anything is left for enjoyable things.”

“This experience was very good for me because it was very difficult for me to figure it all out. I had to make certain sacrifices that I wish I didn’t, but this will be very good for me to do because I will have to do this in my life. I’m very interested to know if I could actually follow this budget strictly. If I was living in this exact situation, I would need to figure out where I could make cuts without causing me too much stress/harm. This was a really great experience and it made me think really hard about this. I would definitely need to find cheaper car insurance becuase as of now that costs me a ton of money.

”

“Overall this is crazy to think about if you only have that much for your budget you have to make it work because you don’t have anywhere else you can just get money to buy what you need. ”

“This experience was really eye opening for me because I knew I wass broke and likely wouldn’t be able to afford much other than necessities but on this budget I literally can’t even afford a car. I don’t drive as of right now and I’ll likely and up in New York (the city or nearby) so I won’t really need one anyways but still. I cut down every expense that I could while still leaving some money for clothes and entertainment because sometimes I can’t make it through the month without a coffee and I figured that the clothes would add up throughout the year so it wouldn’t be one $20 item of clothing a month but rather a new pair of shoes or a hoodie once a year. I also figured the same with entertainment like I could go to a movie every other month or 1 or 2 concerts a year.”

“What surprised me was how many “wants” (i.e. clothes, eating out, entertainment, etc) I had to cut from my budget to fit the $2,386.25 limit. Wants are unrealistic with this income, and it’s clear that when I make this amount, I have to be judicious with my spending in order to prioritize my savings and investments. ”

“It was rough. I had to go to the cheapest housing and car options I could find, and cut on car insurance, groceries, insurance, etc. I could survive on this but it would not be fun.”